MoneyGram international’s Pamela Patsley would rather not talk about the elephant in the room.

Sure, she was No. 6 on Fortune’s highest-paid women executives list in 2009. Yes, her salary and options total something close to $18 million annually. But Moneygram’s petite, 54-year-old chairman and CEO insists that, for her, it has never been just about the money.

“It’s not a measure of someone’s success,” Patsley says of her paycheck. “It has not been my measure.”

Maybe not. In her business, running one of the world’s largest cash-transfer firms, however, money is what makes the world go around. And since Patsley took the helm as the turnaround CEO in 2009, MoneyGram has been hitting its stride.

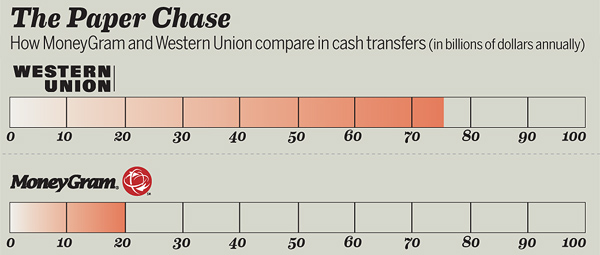

The company boasts annual revenue of $1.2 billion and 244,000 agent-locations around the globe. That’s more than the twice the number of locations of McDonald’s, Starbucks, Subway, and Wal-Mart outlets combined.

Earlier on this particular morning, Patsley was broadcasting one of her quarterly live “town hall” meetings. The Q&A sessions are her way of keeping in touch with the Dallas-based company’s 2,600 employees spread across 23 international offices.

MoneyGram moved its corporate headquarters to Dallas last fall, after 70 years in Minneapolis. Speculation was rampant that its new CEO would choose Big D because her business roots and home are here. Patsley, a St. Louis native who moved here in 1982 to work as an accountant and auditor for KPMG Peat Marwick, said she loves the energy of doing business in Texas, and the diverse mix of public and private companies in Dallas.

It doesn’t hurt that 3,695 of MoneyGram’s agent locations are in Texas, and that others on the company’s management team hail from Dallas.

While North Texas made a logical choice for the headquarters operation, don’t count on Patsley centralizing all of the company’s operations in its two floors at 2828 North Harwood Street. Before the move, most every function—except for some call-center and back-office services in Denver, plus some local and regionalized sales and service operations—were located in Minneapolis.

“That was their culture,” she says. “Minneapolis is where it was based, and every next job was going to be there. I have a different view. In today’s market you don’t need to have that. My philosophy is not to pick a place for the headquarters and say that the back office, development, and IT all needs to be there. It’s not what our business calls for, and it’s not efficient for our business.”

The new Uptown office employs 103; Patsley expects that number to hit 170 by early next summer.

“I was just in Minneapolis this week and we have way more employees [approximately 740] there than here,” she says. “I expect that to continue for a while, or forever.”

Ticking Time Bomb

Back in July 2007, MoneyGram’s stock was trading at $30 per share and the money-transfer business was booming. At that time, CEO Philip Milne and top management told analysts that despite the company’s investments in mortgage-back securities, its investment portfolio was doing just fine. That all changed in January 2008, when $860 million of bad investments, including assets backed by subprime mortgages, bit MoneyGram in the behind.

During Milne’s four-year tenure, MoneyGram lost nearly 90 percent of its market value and its stock came close to being delisted on the New York Stock Exchange, according to a Minneapolis Star Tribune news article.

In March 2008, at the height of the financial crisis, the company completed a recapitalization, or a restructuring of its debt and equity, that would begin steering it back on course. Private-equity firms Thomas H. Lee Partners and investment bank Goldman Sachs Group purchased MoneyGram preferred stock for $760 million, which was convertible into 79 percent of common stock. Goldman also pitched in $500 million for debt financing.

The liquidity event predates Patsley, who was enjoying a brief “retirement period” before a search firm hired by THL and Goldman Sachs contacted her about turning MoneyGram around. She joined the company in January 2009 as executive chairman of the board, and became its CEO in September 2009.

“The opportunity of MoneyGram and the industry it was in was very exciting to me,” she recalls. “It was a chance to leverage everything I’ve done, but yet not be the same. It was an opportunity to build out a team, re-energize the company, fix it up, and leave my mark on it—hopefully leave it with a great and amazing culture and take it forward.”

Midas Touch

Patsley was no stranger to the financial-services industry. After leaving KPMG in 1985, she became CFO of First USA Inc., a Dallas-based bank-card company that went public in 1992. She then served as president and CEO of Dallas-based Paymentech Inc., a credit-card processing subsidiary of First USA that also went public.

Mike Duffy, whom Patsley hired as chief operating officer at Paymentech in 2005, describes his former boss as strong, tough, and compassionate. Whatever Patsley touches turns out golden, he says.

“The first thing I did when she joined MoneyGram was buy a ton of stock,” says Duffy, now president and chief executive at Chase Paymentech. “She’s a winner.”

After Paymentech was acquired by First Data Corp. in 1999, Patsley oversaw FDC’s $3 billion (revenue) merchant-processing business

until 2002. Her last post before MoneyGram was leading FDC’s global expansion as president of First Data International, where she worked in Paris, France, for two years until 2007. In 2006, First Data spun off Western Union—which happens to be MoneyGram’s No. 1 competitor.

When Kohlberg Kravis Roberts acquired First Data in 2007, Patsley says she decided to fold her cards and take her chips off the table.

“My son was a junior in high school that year, and it was kind of a nice time to step back and figure things out,” she says.

She was already serving on several public-company boards—including those of Texas Instruments, Dr Pepper Snapple Group, Molson Coors Brewing Co., and MoneyGram–and figured she might join another board or continue working with private-equity folks such as Boston-based Advent International. Retiring at age 50 probably wasn’t a realistic goal for someone as competitive as Patsley.

As the daughter of two schoolteachers, she says she’s not sure when the lure of the corporate world took root. At the University of Missouri she thought she wanted to study math, like her dad, but veered down the numbers path to accounting. She rejects the idea that her gender has afforded fewer career opportunities than her male counterparts.

“How could I possibly feel that?” she asks. “Let’s be clear. I have met plenty of unenlightened people along the way, some subtle and not so subtle. You know, that’s life. Whether it’s a male/woman, female thing, or sensitivity to ethnicity, I mark it up to not being very bright.”

Those close to Patsley describe her as energetic, communicative, and approachable—and someone who doesn’t need a lot of sleep.

Wayne Sanders, board chairman of the Dr Pepper Snapple Group, met Patsley in the mid-1990s, when both were serving on the Molson Coors Brewing board. He recruited her to the Dr Pepper board, and they also serve on TI’s board together. Sanders says that people can underestimate Patsley, in part, frankly, because she’s a woman in business. But once she starts talking, he adds, that changes.

“Usually she is the smartest one in the room,” says Sanders, the former chairman and CEO of Kimberly-Clark Corp. “She’s serious and dedicated and there to do the right thing for the shareholders, but she is someone you have a lot of fun with while doing this. She has a great sense of humor, and she’s not the kind of person who takes herself too seriously.”

Rising Star

Patsley attributes her steady career build to desire, hard work, and the support of her husband, Gary, who retired 17 years ago from the financial-services industry. His involvement “eased a worry” that things were well tended to at their Highland Park home.

Although some might shy away from a company in crisis, Patsley says it’s been “fun” pulling Moneygram back from the brink during an economically challenging climate.

However, she contends, MoneyGram wasn’t on the brink because of a bad business model—merely because of bad investments that weren’t worth the paper they were printed on.

“What caused MoneyGram these extreme financial challenges and created the situation for Goldman and THL to come in and do the leveraged recapitalization had nothing to do with our core value-creating business, which is money transfer and emergency bill pay,” she says. “It had to do with our investment portfolio. All through this the core business kept growing. There were lots of exiting things about it

for me.”

From the get-go, her strategy was to boost the culture and focus on key initiatives: double-digit transaction growth, double-digit constant-

currency revenue growth. Continuing to grow the agent network and expanding the operating margin and, if things went really well, moving beyond the 2008 recapitalization and converting those preferred shares into common stock.

So far, so good.

In the second quarter of this year, MoneyGram reported a 15 percent boost in money-transfer transaction volume, an 11 percent increase in money-transfer fees and other revenue on a constant-currency basis, and a 20 percent jump in global agent locations over the prior year. Revenue also increased 9 percent to $310 million, compared with $283.9 million in the second quarter of 2010.