After ticking off the virtues of the refurbished tower—once the U.S. headquarters for Nortel Networks—the developer was surprisingly frank about his desire to lease up the building, which was just 23 percent occupied. And to lease it up fast.

“This real estate cycle has been one of the most prolific of my career, and it feels late to me,” Cawley told the brokers. “So, we want to be aggressive and get the building leased while we still have a good market. Cycles are hard to predict, but I know one thing: They don’t last forever. And prudent owners are focused on occupancy.”

Cawley’s candor at the early-evening event in January—which, full disclosure, was intended to launch the 2017 D CEO Real Estate Annual—reflects the mood these days of many in the industry about Dallas-Fort Worth’s current commercial real estate boom. Now in its seventh year, this “up” cycle is longer than previous North Texas expansions, causing observers to question—and many to worry about-—how long it can last.

As 2017 began, the local commercial real estate industry, renowned for its optimistic nature, still seemed to be firing on all cylinders. Last year, after all, was a spectacular one for the business in DFW, with solid job growth—the requisite for continuing strength—and what appeared to be tight, balanced markets across the board. “I’ve been here 41 years, and I’ve never seen the DFW market in better shape,” says Bud Weinstein, an adjunct business professor at Southern Methodist University. “The economy is stronger than it’s ever been, and it’s a lot more diversified than it was 40 years ago.”

Weinstein’s alluding, of course, to a period that culminated with the great real estate crash of the mid-1980s, when cheap money and massive overbuilding, tax reform, and plunging oil prices triggered one of the region’s ugliest downturns ever. It’s a memory that still haunts commercial real estate veterans, who nonetheless insist that, these days, things are different. Phil Puckett, a broker with CBRE who represents office tenants, says Dallas’ organic job growth and attractiveness to relocating companies set the current expansion apart. “Dallas really is a new city,” says Puckett, who is one of D CEO’s Power Brokers for 2017. “It’s just so different now.”

Puckett’s view is echoed by CBRE’s Jack Fraker, another ’17 Power Broker who lived and worked not only through the 1980s downturn, but later through the bursting of the tech/telecom bubble, the 9/11 shock, and the last decade’s Great Recession. Fraker contends there are further checks against a severe downturn today thanks in part to the “institutionalization” of commercial real estate ownership, as well as the widespread availability of more sophisticated information about market trends. “Each successive bust creates more controls in the system, creating stability,” he says.

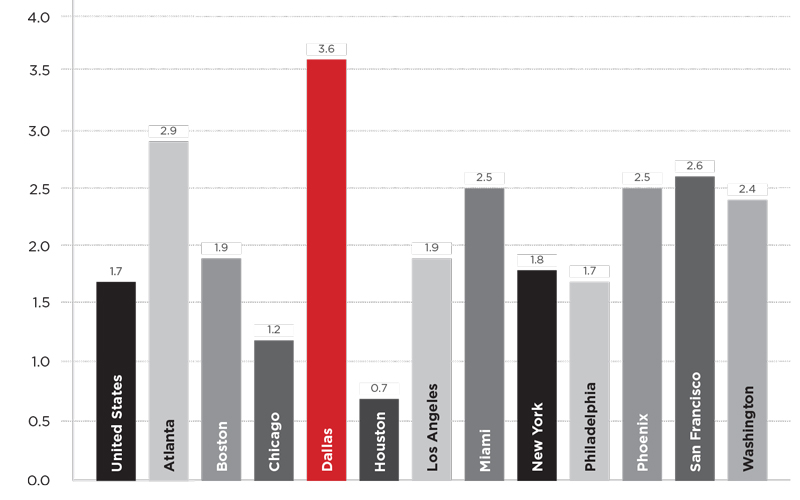

Jobs, Jobs, Jobs

Total nonfarm employment, over-the-year percent change, United States and 12 largest metropolitan areas, September 2016

Robust Employment Growth

What’s also bucking up the optimists is the relative restraint of today’s lenders and developers—Puckett says nearly half of all new office space under construction here is pre-leased—combined with the region’s explosive growth in employment and population. Jobs and people, of course, are what make all types of real estate projects successful. The U.S. Census Bureau says that DFW is the second fastest-growing metro area in the country (behind only Greater Houston), and that Dallas County’s population alone has increased by 186,000 people over the last five years.

According to a January report from real estate brokerage JLL, North Texas has added 732,000 jobs since the beginning of the expansion in 2010. That figure includes nearly 115,000 jobs in the last year, a better than 3 percent growth rate. Laila Assanie, a senior business economist with the Federal Reserve Bank of Dallas, says she expects DFW’s “rate of job growth to moderate some in 2017, similar to 2016. It was 4 percent in 2014-2015, and that’s not sustainable over the long-term.” Last year’s job growth here was broad-based across all sectors, Assanie goes on, including construction, healthcare, professional and business services, and financial activity.

Good news like this has many top brokers predicting that the good times will continue to roll. “This current trend seems to have a fair amount of steam left in it, because the national economy isn’t necessarily overheating in terms of GDP growth, which suggest the fundamentals are still in balance with room for more upside,” says Sharon Morrison, an industrial Power Broker and the CEO at E Smith Realty Partners. “Texas in general is well-positioned relative to the rest of the country, because of our favorable business environment and cost of living.”

Others in the industry, however, are quicker to wave some yellow caution flags. Joseph Cahoon, director of SMU’s Folsom Institute for Real Estate, points out that “real estate works on a seven- to 10-year cycle, and we’re in year seven. What inning are we in in this cycle—the seventh? The eighth? We don’t know anymore.” Greg Biggs, a Power Broker with JLL, notes a similar “concern” that the current cycle is nearly played out. “Everybody hopes we’re wrong,” Biggs says. “But we’re preparing ourselves for that eventuality.”

Others in the industry, however, are quicker to wave some yellow caution flags. Joseph Cahoon, director of SMU’s Folsom Institute for Real Estate, points out that “real estate works on a seven- to 10-year cycle, and we’re in year seven. What inning are we in in this cycle—the seventh? The eighth? We don’t know anymore.” Greg Biggs, a Power Broker with JLL, notes a similar “concern” that the current cycle is nearly played out. “Everybody hopes we’re wrong,” Biggs says. “But we’re preparing ourselves for that eventuality.”Jeremy Zidell of The Retail Connection is concerned as well. As reasons for his caution, the retail Power Broker cites rising interest rates, the increasing cost of land, ever-higher building costs, and record or near-record leasing rates. “We’re coming into a critical measuring point to understand how long the cycle will last,” he says. “It’s had a really long heyday, and no one thought it could last forever. Part of me thought that it would have already ended.

“There’s a recalibration on the horizon, but it will be nothing like 2008-2009,” Zidell hastens to add. “It will be just a minor softening—not catastrophic.”

So, what would cause such a softening? When might the correction start? And, what would it look like?

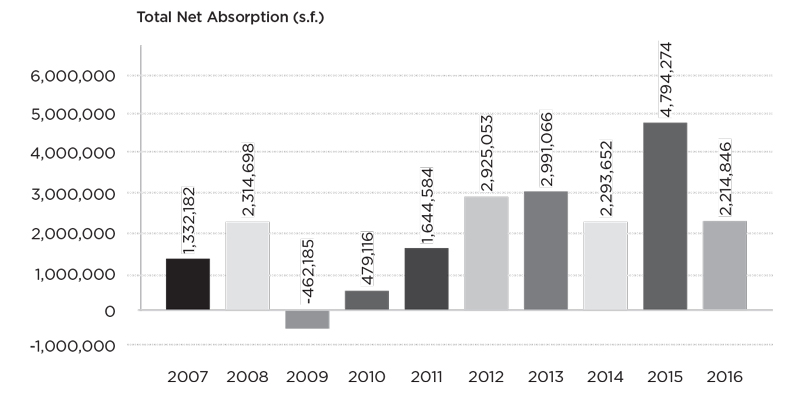

Dallas Offices: Declining Absorption…

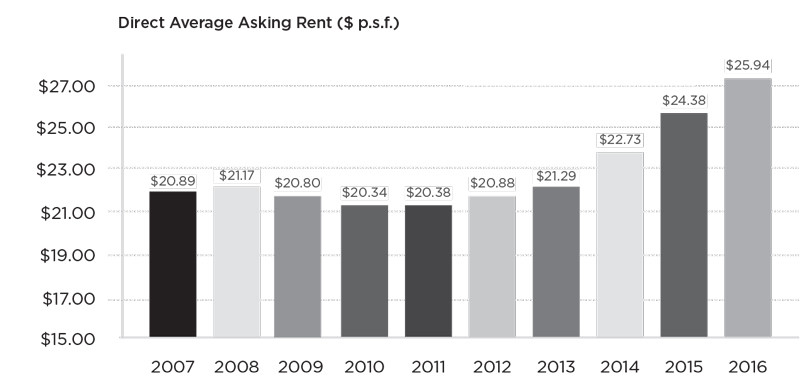

… And Higher Rents

Moving The Chess Pieces

Cahoon of SMU and the Fed’s Assanie say the earliest, most obvious sign of a contraction will be slowing job growth. North Texas “is a leader in job growth in the country, but how long does that hold on?” asks Cahoon. He points out that Collin County has been the biggest beneficiary of recent employment expansion, with its giant relocations or consolidations by companies like Toyota, Liberty Mutual, and State Farm. “People are bullish about 2017 in terms of job growth, but beyond that there’s a lot of uncertainty,” he says. “These deals have been known for a while, and you can’t expect the same pace to continue. I question whether we’ll see the same intensity going forward.

“Are we just the beneficiary of moves out of California?” he asks. “Eventually the chess pieces will stop moving.”

Cahoon says he’s especially “nervous” about the resilience of the multifamily sector in DFW, which has been the nation’s No. 1 market for apartment building. While local leasing and occupancies are at record levels—and 30,000 more units are expected to open this year—some fear multifamily rents have soared too high, especially for millennial renters with relatively low salaries and crushing student-debt burdens. “The strong rate of rent growth in DFW is likely unsustainable,” agrees Assanie. In addition, “financing for multifamily projects is becoming more challenging to obtain.”

Indeed, higher interest rates and tougher underwriting standards by lenders could begin to affect all DFW property types, no matter how well they’ve been performing. And, no doubt, most have been performing well. Median sales prices for existing single-family homes here, for example, which are up 40 percent over the last four years, now are reaching record levels. Nathan Orbin, an industrial Power Broker with JLL, says occupancy, absorption, and rents in that sector all are strong in DFW. Data-center Power Broker Bryan Loewen of Newmark Grubb Knight Frank sees continued solid growth for that niche sector in North Texas this year. With occupancy and new construction at record highs, says CBRE retail Power Broker Karla Smith, “It’s a good time to be a retail landlord in Dallas.” And office-leasing gurus like Fletcher Cordell, a Power Broker with Transwestern, cite that sector’s continuing vibrancy in DFW, with pent-up demand for top-tier space, rents at all-time highs, and a mostly balanced market.

Even so, observers agree, there are a number of warning signs that could portend the boom’s end. Single-family homes could soon be overvalued, causing DFW to fall off the list of the nation’s most affordable home markets. Higher rents and the increasing cost of land and building here soon could cause a headache for industrial and retail owners and tenants. And a January report from Cushman & Wakefield said that an avalanche of new office space is set to hit the North Texas market this year—despite the fact that, according to JLL, net leasing of office space plummeted in 2016 by 50 percent.

In addition, experts caution, some “macro” trends could also spell trouble for the up cycle. Among them: a tariff war with Mexico, a major DFW trading partner; deterioration of the already-struggling Dallas public schools system, affecting the area’s future labor force; higher materials costs and a continuing lack of skilled workers in the building trades; and inadequate planning for roads and other infrastructure, especially in “hot” spots like Plano’s Legacy West development. “If the infrastructure gets so overloaded, that could be one of the things that slows us down,” says Puckett of CBRE.

There are other warning signs as well, adds Cordell, the office broker for Transwestern. “If general contractors become more available to bid jobs, that would be a bad sign,” he says. “Or if you see tenants contracting in the market, obviously, or tenants sticking to their guns on certain contractual obligations,” pushing back against landlord demands.

Taking all these eventualities into account, JLL’s Biggs says, lenders as well as developers are increasingly cautious about spec office projects, and landlords are paying more and more attention to costs and rents, especially in the rising interest-rate environment. Left unchecked, says Cordell, the cumulative effect of the trends could tarnish DFW’s long-standing national reputation as a reasonably priced jobs and population magnet, particularly with respect to the housing sector.

“With the tight housing market and housing prices rising faster than the state and national averages, that’s something that people involved in the next big relocations will be keeping an eye on,” Cordell says. “If you’ve been pitching Dallas for its ‘low cost of living’ compared to cities like Phoenix, Atlanta, Salt Lake City, and Charlotte, that might have been at the top of the fold on your brochure before. Now, it might be more at the bottom of the fold. If it was No. 1 before, now it might be No. 4. It’s not horrible. It’s just not the best.”

Finally, there’s always the “wild card” to consider—the unforeseen factor that could harm the local and national economies, curtailing DFW’s real estate expansion in the process. Walter Bialas, a researcher at JLL who says a correction could come as early as 2018 or as late as 2020, suggests the trigger might be “something we’re not thinking about, like European interest rates.” Cahoon of SMU agrees about the unpredictability. “It only takes one catastrophe or shock to the economy to change things,” he says. You can’t underestimate “the impact of global news on markets,” he adds, “or how quickly it can grab hold, in terms of fear.”

All of which may explain why Bill Cawley, the developer of Lakeside Campus Tower, was so eager that January evening to give away those $100 bills.

Biggest Brokerages

The biggest commercial real estate firms in North Texas, ranked by the number of local brokers.

Our 2017 study of the largest brokerages involved 72 firms with a total of 1,720 North Texas brokers, who are defined as licensed professionals helping to produce revenue for their firms. The top five firms in this study—CBRE, JLL, Cushman & Wakefield, Transwestern, and Colliers International— finished in the same order that they did last year. Marcus & Millichap vaulted into the sixth position, up from No. 9 in 2016. Other solid gainers this year included Stream Realty (jumping to No. 10 from No. 15 last year) and Venture Commercial (No. 14, after ranking No. 16 in 2016). Firms making their debuts on the list this year were Younger Partners, Lincoln Property Co., and Morrow Hill. [EDITOR’S NOTE: THE VERSION OF THIS CHART THAT APPEARED IN THE MARCH 2017 ISSUE OF D CEO MAGAZINE OMITTED NAI ROBERT LYNN.]

| 2017 Rank | 2016 Rank | Firm | 2017 Local Brokers | 2016 Local Brokers |

|---|---|---|---|---|

| 1 | 1 | CBRE | 223 | 223 |

| 2 | 2 | JLL | 200 | 197 |

| 3 | 3 | Cushman & Wakefield | 101 | 110 |

| 4 | 4 | Transwestern | 83 | 93 |

| 5 | 5 | Colliers International | 70 | 55 |

| 6 | 9 | Marcus & Millichap | 62 | 45 |

| 7 | 6 | NAI Robert Lynn | 55 | 53 |

| 8 | 8 | Henry S. Miller Brokerage | 50 | 50 |

| 8 | 7 | Swearingen Realty Group | 50 | 52 |

| 10 | 15 | Stream Realty Partners | 47 | 32 |

| 11 | 10 | Jackson Cooksey | 43 | 43 |

| 12 | 16 | Newmark Grubb Knight Frank | 40 | 30 |

| 12 | N/A | Younger Partners | 40 | N/A |

| 14 | 16 | Venture Commercial | 36 | 30 |

| 15 | 13 | The Retail Connection | 35 | 34 |

| 16 | 11 | Mohr Partners | 33 | 37 |

| 17 | 16 | Avison Young | 30 | 30 |

| 17 | 19 | Bradford Commercial Real Estate Services | 30 | 25 |

| 17 | 12 | Weitzman Group | 30 | 36 |

| 20 | 19 | Rubicon Representation | 25 | 25 |

| 20 | 24 | Vitorino Group | 25 | 20 |

| 22 | N/A | Lincoln Property Co. | 24 | N/A |

| 23 | N/A | Morrow Hill | 23 | N/A |

| 24 | 24 | Edge Realty Partners | 22 | 20 |

| 25 | 24 | Peloton Commercial Real Estate | 20 | 20 |