After her husband died, Jo Hopper spent eight years fighting the bank administering the estate. She won a record-setting judgment. But will JPMorgan Chase ever pay up?

Jo Hopper is sitting in her lawyer’s office in North Dallas, slowly, calmly telling the story of how she believes the nation’s largest bank tried to take away her home and her possessions, and destroy the relationship she had with her stepchildren. Her saga began eight years ago this month at Medical City Dallas. There, on January 25, 2010, Max Hopper, who had been a titan of early corporate information technology, a genius who had led the development of American Airlines’ AAdvantage program and its SABRE reservation system, died. Max had been in good health but suffered a stroke the day before. He was 75.

“I remember at the hospital,” Jo says, “I kept saying to the doctor, ‘What else are you going to do? You do not understand. This is Max Hopper. He cannot die.’ I would not accept it. Even today, it is hard to fathom.”

Spread his wings: Max and Jo had lifetime passes to claim available seats on American flights, but his son thought Jo mightbe using his Max’sAAdvantage miles.

Jo was 62 when the man she’d been married to for 28 years died. She has spent much of the ensuing eight years locked in a legal battle over $19 million in assets she and Max jointly owned. Her opponent: Manhattan-based JPMorgan Chase, the largest bank in the country, with $2.6 trillion in assets under management. Jo and her stepchildren hired the bank to administer Max’s estate in 2010, after Max died without a will, leaving his assets in financial limbo. But soon after JPMorgan had collected its $230,000 fee for the estate administration, something went horribly wrong between the bank and the beneficiaries. Lawsuits ensued. Jo sued the bank. The bank sued Jo. Jo sued her stepchildren. The stepchildren sued Jo. The stepchildren sued the bank. And so on.

In September of last year, a jury finally heard the case. It ruled in favor of the family with a historic and headline-grabbing $8 billion award against JPMorgan. That was the largest punitive award ever in Texas. The jury’s ruling was so abnormally large that attorneys representing the plaintiffs weren’t even sure how to calculate it—the initial guess of $4 billion eventually gave way to the higher $8 billion estimate.

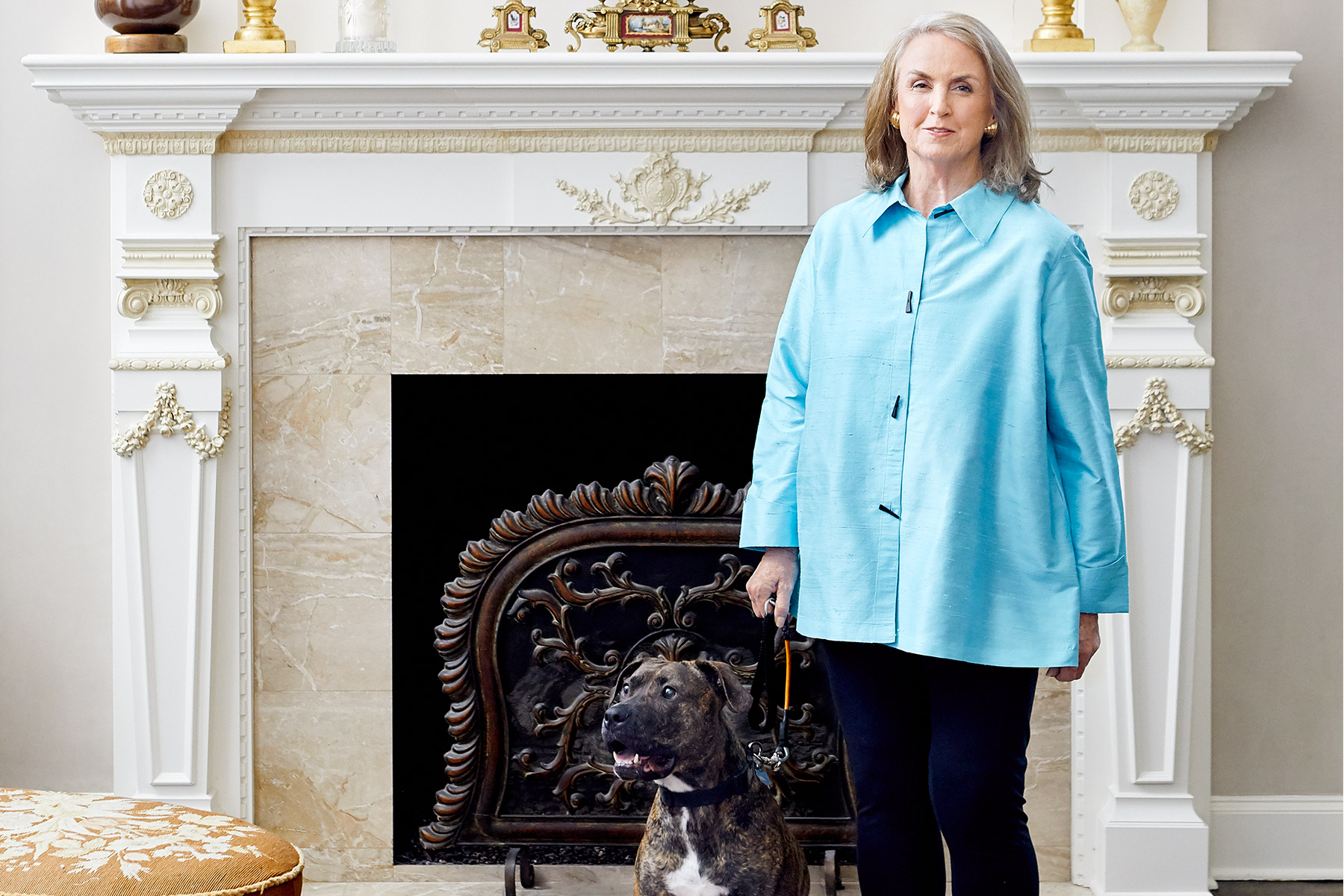

Jo has claimed in her court filings to be a widow wronged by the bank, but she is no frail, little old lady. In 2007, she was diagnosed with stage 4 lymphoma and given six months to live. She has been in remission for almost eight years and today stands steady at 5 feet 4 inches. On the day we meet, she’s wearing a flowing white top and black pants. Silver bracelets adorn her wrists. Her gray hair is pulled back tightly into a bun. Her attorney, Alan Loewinsohn, is here sitting beside her. But Jo leads the conversation.

As she weaves this narrative of endless court fights, Jo hands over pages of documents. There’s a pamphlet produced by JPMorgan called “The Well-Prepared Family” that explains how to choose an executor. She has highlighted the part that says an executor “is legally responsible for preserving the value of the estate until it is distributed” and another passage that says, “An executor is obligated to act in the best interest of the estate’s beneficiaries.”

Next comes a printout of a job listing at JPMorgan in Dallas. They’re hiring someone in asset management to oversee trusts and estates. “I’m looking for a job,” Jo says. Her attorney laughs. “No, really,” says the Nashville native, née Jo McClendon.

Finally, she hands me a paper written by a professor at Ohio State University called “The Stepmother’s Role in a Blended Family.” Jo has highlighted a paragraph noting that “there have been more than 900 stories written about evil or wicked stepmothers.” Cinderella and Snow White are just two among them.

Better days: Max and Jo were married for 28 years.

The family feud between Jo Hopper and her stepchildren—61-year-old Oklahoma City physician Stephen Hopper and Laura Hopper Wassmer, the 55-year-old mayor of Prairie Village, Kansas—is a big part of this story. But Jo’s version is different from the bank’s. The bank has based its legal defense on the toxic relationship between Jo and Max’s children. It claims the family would have had no complaints about its services had the three of them just found a way to get along. The three heirs, in turn, allege the bank botched Max’s estate—committing fraud and possibly a felony in the process, as well as driving a wedge between stepmother and stepchildren.

Fraud. Felony. How did a jury come to believe that a bank that has been part of the bedrock of the American financial system since 1871 might have done such things to a widow and her stepchildren? And what made that jury so angry—or so concerned that what happened to the Hoppers could happen to any of us—that it insisted on making an unprecedented statement with its verdict? To be sure, Jo Hopper’s story is a good one. But good enough to deserve $8 billion?

JPMorgan would never have been hired to manage Max Hopper’s estate, if Jo had her way. She would have done it herself.

All four wills that Max drafted before his death, but never signed, said Jo should serve that role. She’d handled the family finances for decades, and, like her husband, she’d worked as an executive at American Airlines, once managing a staff of five systems analysts, a personal assistant, and a multimillion-dollar budget.

Plus, the law, Jo figured, was easy to understand. When someone dies “intestate,” as a lack of a will is called, Texas law stipulates that the decedent’s share of the community property—anything Max and Jo owned jointly—will go half to the surviving spouse and half to the decedent’s children. Any property owned outside of the marriage should go two-thirds to the children and one-third to the surviving spouse. “So all we had to do,” Jo says, “was go through the assets, divide everything by two and then divide again by two. Then we’re out of here.”

courtesy of Jo Hoppercourtesy of Jo HopperMax didn’t grow up to become a cowboy, but he was a maverick in his industry. Before that, he spent time in the armed services.

Stephen and Laura didn’t see it that way. In March 2010, two months after Max died, the Hoppers met at the $2 million, 8,000-square-foot Preston Forest home on Robledo Drive that Jo and Max had bought in 1997. The children, as Jo calls them, even though they were both adults when she married Max, insisted on hiring JPMorgan as an independent administrator in part because they wanted someone impartial to handle any disputes that might arise. “That’s what the children wanted,” Jo says. “They wanted assurances. So I agreed.”

Days later, the family settled on JPMorgan for the job. The bank was charged with doing what Jo had proposed to do: find all the assets, add them up, divide by two, and divide by two again. But the Hoppers found the process to be too slow. They say the bank didn’t act quickly enough in executing stock options Max owned. They allege taxes were improperly filed. And they say the bank was tardy in responding to other requests to make financial transactions. All of that cost the children and Jo tens of thousands or possibly hundreds of thousands of dollars in lost income, attorneys for both parties have claimed.

Jo and the children placed much of the blame for that on Susan Novak, a 66-year-old JPMorgan executive who had worked on estate cases for nearly 20 years both at JPMorgan and at Bank of America and was the person in charge of the Hopper estate. The family painted Novak as inexperienced, noting that she had worked on only one intestate case before in her career. The bank has said Novak did her job flawlessly. Novak, in court, said that although she had 25 to 30 other estate cases to manage, she spent 70 percent of her time—about 1,800 hours per year—working on the Hopper estate.

In many of those hours, court records indicate, she was trying not to get involved in the mistrust between Jo and her stepchildren. To cite just one example out of many: early on in the bank’s administration of the estate, Stephen contacted the bank to complain that he believed his stepmother might have been using Max’s share of American Airlines AAdvantage miles—a share that, legally, would belong to the children.

In fact, there were no miles needed. Jo and Max were R-class flyers on American, meaning they both had a lifetime pass to claim available seats on flights. That was thanks to Max’s long tenure as a top executive at the airline. The children claim that Novak never told them about the R-class status, never cleared up the issue of potentially missing AAdvantage miles. Without information to the contrary, the children continued to believe—until the facts came out in court filings—that their stepmother was taking trips using miles that belonged to them.

(Novak retired from JPMorgan in the spring of 2017, but she represented the bank in an official capacity during the jury trial. JPMorgan declined to make any individuals involved in the case available for comment for this story.)

Max Hopper was a titan of early corporate information technology, a genius who led the development of American Airlines’ AAdvantage program and its SABRE reservation system.

The children allege that there were other imbalances that also put them off. For one, the bank flew Jo to New York and sent her, gratis, to The Phantom of the Opera, trying to woo her to open a wealth management account. She did, and as assets were divided and released to Jo, her share was transferred to a JPMorgan investment account. Over time, that money accumulated to more than $4 million. The children were never told about the New York trip. They also alleged that they weren’t told that Jo wasn’t asked to pay any of the $230,000 fee JPMorgan charged to administer the estate.

In January 2011, Jo says that Mike Graham, her probate attorney at the time, sent an offer to Novak saying Jo wanted to buy all of the personal property that had not yet been distributed by the bank. That included Max’s collection of 6,700 putters, 900 bottles of wine, the furnishings in her Preston Forest home, jewelry, and more. Basically, everything except the house.

Novak replied to Graham but never notified the children of the offer, Jo says. Two more emails from Graham followed. No counteroffers came back. “We assumed the children had rejected the offer,” Jo says.

This pattern continued. Family members mistrusted each other. Family members contacted the bank with various allegations. The bank didn’t share those allegations with both sides. Mistrust festered.

By the summer of 2011, Jo’s attorneys had become so concerned with the bank’s lack of communication that they advised her to close her wealth management account. The $4 million she had invested with JPMorgan promised to eventually bring a nice return to the bank. Financial institutions typically charge a fee of just under 1 percent of the total assets in accounts worth more than $1 million. Meaning that JPMorgan, in less than five years, could have made more off of Jo’s wealth management account than it would make administrating Max’s estate. (The bank says it never collected more than $5,000 in fees from Jo’s account in that first year.)

As soon as the account was closed, Jo says, the bank turned against her. “The relationship became adversarial,” she says. “Suddenly, if the children objected to something I wanted, the bank sided with the children.”

That’s what seemed to happen when a dispute arose over Jo’s Preston Forest house. The same summer that Jo closed her wealth management account, she asked the bank to divide the ownership of the house evenly between her and the children. Jo had already exercised her homestead rights on the property, meaning that as long as she could make the payments on the house, she would have the exclusive right to live there. Now she wanted the home divided into equal ownership. The children, though, wanted cash for their half—Max’s half—of the home.

Max and Jo’s $2 million, 8,000-square-foot Preston Forest home.

The way the children, and their then attorney, Gary Stolbach, figured things, dividing ownership in a home they could not use and could not sell so long as Jo lived there (which was her guarantee under the homestead rules) was not a fair division of the estate. The children wanted the property “partitioned,” meaning they would get compensated for their half of the home and Jo would then own it outright.

There’s a lot more brain-rattling legal nuance involved from there, but the important thing to know is that this “partition” was a novel legal theory Stolbach had floated. Jo says such a thing had never been done before to a widow or widower in Texas, and the bank had no obligation to go along with it. JPMorgan, in fact, had the right to simply declare the home equally divided, which is what Jo wanted and what the bank also initially said it wanted.

“The bank was appointed as the independent administrator,” says James Bell of James S. Bell PC in Dallas, who represented the children during the jury trial but is no longer an attorney on the case. “In an independent administration, it means the bank can do whatever, whenever, however it wants to do. It can split the assets how it wants as long as it is not violating the statutory guidelines. And for over a year the bank could have divided that house how they saw fit in accordance with the law. But they just didn’t do it until there was litigation.”

The litigation was initiated by Jo. She filed a lawsuit against both the children and the bank in late September 2011. From the children, she sought a court declaration that a partition was not legal. From the bank, she sought a declaration that the bank had breached its contract with her, that it had committed fraud and breach of fiduciary duty by misrepresenting its expertise in handling cases like hers and by failing to properly communicate with her and the children. Further, she sought the bank’s removal as independent administrator.

courtesy of Jo Hoppercourtesy of Jo HopperThe Collector:Max and Jo’s home held Max’s collection of 900 bottles of wine and 6,700 putters, which Jo tried to buy from the estate.

After it was sued, the bank asked the probate court to declare that it had the right to do what the children had asked, even though it had previously told Stephen and Laura that it preferred to do what Jo wanted—divide ownership equally. From there, JPMorgan doubled down. The bank also asked the court to affirm that it not only could “partition” the house—forcing Jo to compensate the children for their one-half interest in the house—but it could force Jo to sell her house to a third party, at a price she could not negotiate.

The bank acknowledged that because Jo had exercised her homestead rights, it could not kick her out of the house. But it maintained that it still had the right to make her a tenant in her home, which someone else might own. The bank further said that it had the right to take back some of the assets it had already distributed to Jo and make her use those assets to buy out the children’s interest in the Robledo home.

Here’s how the $8 billion jury seems to have heard those facts: the largest bank in America told a court that it would consider forcing the sale of a widow’s home over the widow’s objections.

“I couldn’t believe it,” Jo says, speaking in Loewinsohn’s office. “Max and I owned that house. The probate code doesn’t allow for a partition.”

There’s a book on the table beside her—Johanson’s Texas Estates Code Annotated. It’s a 1,661-page reference book on probate law in Texas that Jo bought in 2011. That year she spent Thanksgiving reading it. All of it. Every page.

“One juror told me, ‘If the bank didn’t care about Jo Hopper and the money she had, why would they care about us when we don’t have that kind of money?’ ”

Jo picks up the bulky book with one hand and flips it open to a page she has marked. It shows the probate code’s stance against partitioning a home after the death of a spouse. “It’s right here. It’s the law,” she says. “The bank knew that. But the bank was bullying me, trying to emotionally break me. This tactic was unbelievable and unprecedented as far as I could find. They were going to sell a widow’s home.”

Initially, the bank’s stance was upheld, in part, by the probate court. But eventually, the probate court modified its ruling, and the litigation over the house concluded in two ways. In June 2012, the bank decided to divide the house ownership in equal interests, as Jo had wanted all along. Then, on December 3, 2014, the three justices who preside over the Eighth District Court of Appeals issued a 26-page ruling that chided the earlier probate court and declared the novel partition theory unlawful. Jo had her house; the children had half a mortgage.

JPMorgan is not wrong about the family’s blood feud. The bank says it tried to get the sides to come to terms before the issues about the house ended up in court. “We continually urged the family to reach an agreement on the division of the home and personal property,” says Greg Hassell, a spokesman for JPMorgan. The children declined to comment on specific questions regarding their stepmother. But attorneys who have represented both Jo and the children say neither side is speaking to the other, except through their lawyers. That might have something to do with a handful of nasty court filings that came out after Jo sued JPMorgan and the children in September 2011.

In one such filing, from 2016, the children said that they “have been antagonistic to Mrs. Hopper (personally, legally, or in both contexts) for nearly six years. Beginning with Max Hopper’s sudden death in 2010, distrust marred the relationship between the Heirs and Mrs. Hopper. This uneasy relationship is precisely what prompted the Heirs to insist Max Hopper’s estate be administered by a neutral, independent third party. That is what the Heirs believed the Bank to be when they engaged its services as independent administrator in 2010.”

In another filing, from 2014, Jo’s attorneys compiled a long list of things that they wanted to be sure would never be mentioned in front of jurors. Those included:

Jo’s “decision to pay for or not pay for any college related expenses, including tuition, for any grandchild of Max Hopper”; why Jo “did not sit on the front row of Laura Wassmer’s wedding in 1987”; that, when a “document production” on Jo’s behalf in this case was held in a garage in 2012 “it was cold outside, and/or the house was locked so if anyone needed to use the restroom, they had to go down the street to a public restroom”; “Any suggestion that Jo Hopper had any type of romantic relationship with Max Hopper prior to his divorce”; and any “reference to a book entitled How to Marry a Millionaire.”

Jo insists the bank exacerbated that infighting. “I’ll admit,” she says, “there was a crack in our relationship. Anybody who goes through the loss of a father with a stepmother, you’re going to have a crack. But what JPMorgan did was they took that crack and they made it into the Grand Canyon.” But since JPMorgan officials have said in court that the family dynamic was toxic and unsalvageable, and since both Jo and the children sued to have the bank removed as independent administrator, one wonders why the bank didn’t just resign.

The answer to that question, say attorneys for the children, ends with two words: “theft” and “felony.”

“That is the key question you have to ask yourself here,” says Bell, the attorney who represented the children during the jury trial. “Why did the bank not step down as the independent administrator? The reason is if they stepped down, there was a lawsuit naming them, so they would have had to pay the legal fees for that lawsuit out of their own pocket. But if they stayed in the case, they had a war chest to defend themselves with. And the war chest they had just so happened to be an account with my clients’ money in it.”

Independent administrators are allowed to hire attorneys and pay legal fees using assets of an estate so long as they are using those lawyers and fees to represent the interests of the estate. And when Jo sued the bank and the children in 2011, the bank decided to cover the legal costs of defending itself by withdrawing money from an estate account that had nearly $4 million in it. The children claim that money belonged entirely to them.

When the children in turn sued the bank, the bank used that same war chest—the money that would have gone to the children—to fight their claims.

Once the children discovered the estate’s money was being used to pay the bank’s lawyers in the legal fight, they asked for the bank to stop using the account. JPMorgan did not comply. Eventually, the account was drained of all but $100, just enough to keep the account open. Then JPMorgan made its own novel legal move. The estate, as administered by the bank, took out a loan, from JPMorgan, for more than $900,000. The bank, in other words, loaned itself money, indebting the estate in the process.

That was only revealed during the trial when Bell cross-examined the lead attorney for Hunton & Williams, which JPMorgan had retained. Just before closing arguments in the jury trial, JPMorgan decided to forgive the estate that loan amount and pay the $900,000-plus out of its own pocket. But it did not reimburse the estate for the nearly $4 million it had already spent on legal fees.

The six jurors found that JPMorgan had committed something called “conversion” when it took money out of the estate’s account to pay attorney’s fees against the will of the children. “Conversion” is a term of art that means taking something that doesn’t belong to you and exercising control over it even when the rightful owner demands that the something be returned to their control.

“Fiduciaries are entitled to hire counsel,” says Russell Fishkind, a partner with Saul Ewing Arnstein & Lehr in New York and the author of Probate Wars of the Rich & Famous: An Insider’s Guide to Estate Planning and Probate Litigation. “So long as the fiduciary’s goal is to further the interest of the estate and enhance the purpose of the estate, and their fees are reasonable, courts will typically allow the fiduciary to hire counsel and for the counsel fees to come out of the estate.

“The question in this case was, ‘Is that what JPMorgan was doing?’ Clearly the jury thought not. It thought the company was working in its own interests, not in the interests of the estate.”

The children’s attorneys, in an October filing with the probate court, also now say that the conversion they’ve alleged in this case qualifies as theft under the Texas Penal Code. They contend that the theft is a first-degree felony because the value of the property stolen is more than $300,000.

If the court agrees with the children’s attorneys, then the state’s caps on punitive damages—Texas generally limits such damages to two times the amount of actual economic damages—may no longer apply. JPMorgan could face a significant payout to the children and maybe to Jo as well.

Tom Fee, a partner with Dallas-based Fee, Smith, Sharp & Vitullo, told me by phone in early October, “We think we can bust the punitive damage caps in Texas. There is a provision that says if you’re a financial institution and you basically commit a crime, the caps don’t apply.”

Still, Fee and his partner Lenny Vitullo, who was on the trial team for the children, haven’t asked the court to uphold the jury’s huge award—whatever that award might be. Initially, the firm said Jo had been granted $2 billion and their clients had been granted $4 billion by the jury. It even issued press releases to that effect. But, looking more closely at the jurors’ paperwork, it became clear that the jurors had gone further. The six-person panel found that JPMorgan had made malicious breaches in its fiduciary duty to the estate—meaning Stephen and Laura collectively. It awarded the estate $2 billion for that. The jury also found that JPMorgan had committed fraud, for which it gave $1 billion each to Stephen and to Laura. It also awarded the same $1 billion amount to each of the children for negligence on the part of JPMorgan. That’s $6 billion total for the children and $2 billion for Jo.

The bank has suggested the jury award is out of line and will not stand up to judicial review. But, even though Fee believes the award is something more than jackpot justice from a runaway jury, they won’t ask the probate judge reviewing the jury award to uphold the unprecedented award. Instead, they’ve asked for about $75 million, or nine times the actual economic damages they say the children have suffered. “We realize we’re not going to collect the $2 billion,” Fee told me just two weeks before Stephen and Laura asked their attorneys to stop speaking with the media. “So we’re seeking the maximum that the law does allow us to recover. For our clients, this is about more than money. Our clients really wish Chase would take some responsibility here. So we want to back up the jury, back up those citizens who gave their time and attention to this. And to protect other consumers, we believe we need to make this stick.”

The jury verdict in the hopper case came after midnight on September 27. The jurors had deliberated for four hours. As soon as they were done, they sought out Jo, Stephen, Laura, and their attorneys. “They said they felt bad about what Jo had been through,” says Loewinsohn, Jo’s attorney. “One of them told me, ‘If the bank didn’t care about Jo Hopper and the money she had, why would they care about us when we don’t have that kind of money?’ ”

The jurors said the same thing to Stephen and Laura, who agreed to answer a few of my questions jointly, by email. “In talking with several of the jury members after the trial, they commented that they felt we had been bullied by JPMorgan, and that they awarded the huge verdict because they didn’t want other families to go through what we have had to go through,” the children wrote. “They were hoping that the verdict would change the way JPMorgan conducted business.”

Funny thing about that: on the trading day immediately following the early morning jury verdict, JPMorgan Chase stock opened at $93.70 per share and closed up, at $95.18. Either Wall Street figured a company with 243,000 employees and a net income of $24.7 billion could survive an $8 billion payout, or the verdict hadn’t registered at all with investors.

Still, the verdict did generate some bad publicity for the bank. On The Motley Fool Podcast, for instance, co-hosts Alison Southwick and Robert Brokamp bantered about it. “Anyone who reads about this case will be told it’s going to get knocked down in appeals,” Brokamp said. “They’re not going to get $4 billion to $8 billion. The lesson, here, is to get an estate plan. But if you don’t have one, hire JPMorgan. They’ll do a horrible job—”

“And,” Southwick said, “You get your payday.”

That remains to be seen. The probate court will have more hearings on the case early this month, but a final ruling on the historic jury award is likely months, if not years, away. The stepmother that neither Stephen and Laura are speaking to, the stepmother who is no longer in touch with her grandchildren because of this case, she will have to wait. “We fought,” Jo Hopper says. “But we haven’t effected change. Not yet.”

Get the D Brief Newsletter

Dallas’ most important news stories of the week, delivered to your inbox each Sunday.

There was only one pro team that could realistically be lured to town. And after two years of (very) middling results, the Ad Hoc Committee on Professional Sports Recruitment and Retention delivered.

Once the children discovered the estate’s money was being used to pay the bank’s lawyers in the legal fight, they asked for the bank to stop using the account. JPMorgan did not comply. Eventually, the account was drained of all but $100, just enough to keep the account open. Then JPMorgan made its own novel legal move. The estate, as administered by the bank, took out a loan, from JPMorgan, for more than $900,000. The bank, in other words, loaned itself money, indebting the estate in the process.

Once the children discovered the estate’s money was being used to pay the bank’s lawyers in the legal fight, they asked for the bank to stop using the account. JPMorgan did not comply. Eventually, the account was drained of all but $100, just enough to keep the account open. Then JPMorgan made its own novel legal move. The estate, as administered by the bank, took out a loan, from JPMorgan, for more than $900,000. The bank, in other words, loaned itself money, indebting the estate in the process.