Texans tout their state’s prowess in creating jobs, with good reason. Since 2005, the Lone Star State led the nation with a net gain of 2.2 million jobs, propelled in large part by employment growth of 591,500 jobs in Dallas-Fort Worth and 639,900 jobs in Houston. Together, the two bustling metros accounted for 57 percent of Texas’ increased employment.

To gauge how DFW and Houston stack up against other large metropolitan areas, it’s best to look at job growth in percentage terms. Among the 30 largest metros by population, Houston leads at 27.5 percent in the past decade, followed by DFW at 21.3 percent.

The rest of the Top Five are Denver at 17.4 percent, Seattle at 15.2 percent, and Orlando, Florida, at 14.9 percent. The past decade’s weakest labor markets show actual declines in employment, including -5.4 percent in Detroit and -2.3 percent in Cleveland.

We usually hear about local employment growth on a company-by-company basis—new enterprises being formed, businesses relocating from other places, or existing employers expanding their operations. These activities happen all over the country, but why are they taking place with far greater frequency in DFW, Houston, and other Texas cities?

It could simply be a matter of geography and geology. That seems to be the opinion, anyway, in big metropolitan areas that lag DFW and Houston in job growth. They sneer that Texas prospers because an oil industry simply pumps wealth out of the ground. That view, however, can’t tell us why the state’s job-creating machine churned away throughout the 1990s, when low oil prices stifled drilling and production. If not oil, then what? Our research points to the state’s high degree of economic freedom (see D CEO’s January/February 2015 issue).

Economic freedom may seem a subjective concept that’s hard to quantify. In recent decades, however, economists have made great strides in using hard data to measure economic freedom—first for nations, then for states. More recently, Dean Stansel, co-author of the Economic Freedom of North America 2014 report, has applied the well-tested methodology for measuring economic freedom to the 300 largest U.S. metropolitan areas.

Stansel’s work incorporates several dimensions of economic freedom, but the one that most directly relates to job creation involves the labor market. Governments impose rules and regulations that impact hiring practices, pay levels, employment conditions, union membership, entry into occupations, and the ease of cutting jobs when business conditions falter. These measures may be well-intentioned or self-serving, but overall they tend to raise labor costs or impose other impediments that affect the decisions of employers and workers.

Where labor-market freedom ebbs, companies respond by hiring fewer workers or relocating to places with fewer restraints. Where labor-market freedom expands, labor markets operate more freely, and employment usually grows.

Freer is Better

Stansel uses three indicators to calculate metropolitan areas’ labor-market freedom, all of them, to some degree, reflecting state-level policies.

The minimum wage relative to the local per-capita income illustrates the degree to which workers and employers bargain freely in the marketplace. Raising the minimum wage diminishes labor-market freedom, particularly in places with relatively low incomes.

State and local government jobs as a share of total employment gauges the relative size of a metro area’s public sector. The more employment provided by private companies, the greater an area’s labor-market freedom.

AVERAGE PAY HIGHER IN FREER LABOR MARKETS

The percentage of employees who are union members measures the power of organized labor to interfere with pay and workplace practices. Labor markets tend to be freer in states with right-to-work laws, which prohibit contracts that make union membership a requirement for employment.

Combining all three indicators reveals wide gaps in labor-market freedom—on a scale from 1 to 10, with higher values indicating greater freedom. Among the 25 largest metropolitan areas, DFW rates highest at 8.48, followed by Houston at 8.31 (see chart on page 82). New York, Detroit, Seattle, and several California cities are at the tail end of the Top 25, with scores of 5.91 and below.

Looking more broadly at the 100 largest metropolitan areas, we see that the 20 percent with the freest labor markets posted an average job growth of 12.9 percent from 2005 to 2015. As average labor-market freedom diminishes, the decade-long increases in employment fall, culminating at 4.8 percent for the least-free 20 percent.

Faster job creation goes along with lower unemployment. We find that metropolitan areas in the freest fifth had an average unemployment rate of 6.6 percent from 2005 to 2015, compared with 7.8 percent for metros in the least-free 20 percent.

The advantage for freer labor markets shouldn’t be surprising; the interplay between supply and demand makes labor markets more efficient and lowers the costs of hiring and retaining workers.

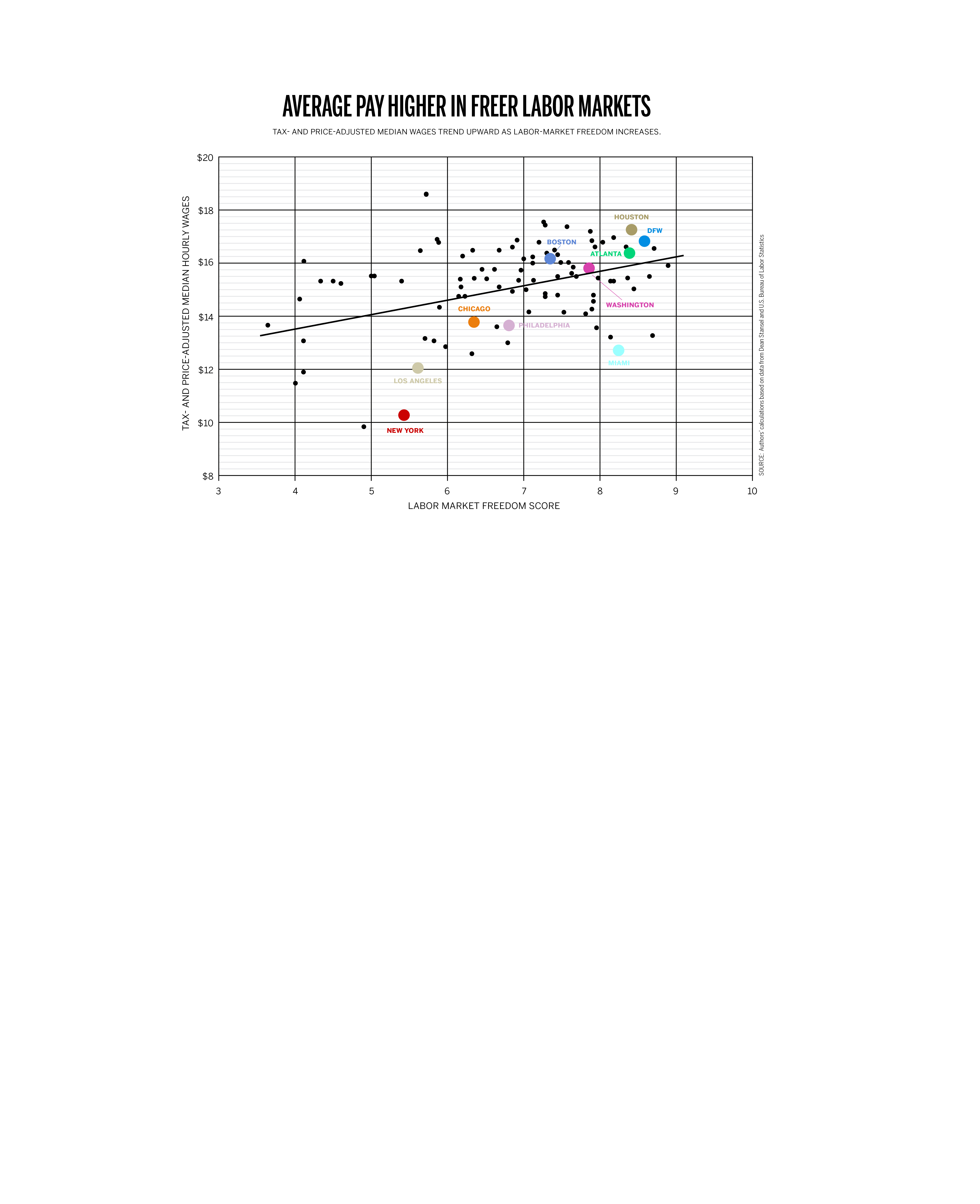

Although labor-market freedom stimulates job creation, some may still worry that it tilts the playing field in favor of employers—for example, wages could be bid down. The data say otherwise, at least when we look at metropolitan areas’ average pay adjusted for the cost of living, including housing, and differences in tax burdens.

Employers in New York City pay high wages, but high taxes and expensive living costs reduce the real value of workers’ median hourly pay to $10.32—the second lowest among the 100 largest metropolitan areas. Los Angeles does only slightly better at $12.08. With low prices and taxes, workers are much better off in the Texas metros—DFW at $16.85 and Houston at $17.27.

In the Top 100 metropolitan areas, tax-and-price adjusted median wages trend upward as labor-market freedom increases (see chart above). This result makes sense: Freer, more vibrant labor markets increase demand for workers, putting upward pressure on after-tax real wages.

What’s more, laws that empower unions don’t do much to raise wages. Among the 100 largest metropolitan areas, the median hourly wage, after adjusting for living costs and taxes, was $15.49 for the top 20 percent in labor-market freedom. The least-free 20 percent had an average wage of $14.12.

How can this be when, after all, a prime purpose of unions is to raise wages? The answer: Organized labor thrives in a political setting hostile to economic freedom, where policies inhibit worker competition and productivity—ultimate contributors to higher wages and job growth.

Freedom at Risk

Labor-market freedom benefits workers and contributes to a growing economy, but it rests on policies that state legislatures or city councils can change at any time. The risk of policies that erode labor-market freedom has grown in recent years as more Americans worry about the plight of the middle class and widening income inequality.

So far, most of the clamor has focused on raising minimum wages. Seattle decided to raise its minimum wage to $15 an hour by 2021—the nation’s highest. A half-dozen other cities have enacted minimums above the federal (and Texas) minimum of $7.25 an hour. Their labor-market freedom will decline in the years ahead, which the data suggest will end up hurting job prospects and wages.

Don’t expect DFW or Houston to jump on this bandwagon. Supported by high levels of labor-market freedom, the Texas metros have enjoyed the best of all worlds—low unemployment, rapid job growth, and higher wages.

DFW Tops in Labor Market Freedom

25 Largest Metro Areas

Dallas-Fort Worth: 8.48

Houston: 8.31

Atlanta: 8.28

Tampa, Florida: 8.25

Miami: 8.14

Phoenix: 8.04

Denver: 7.76

Washington: 7.76

San Antonio: 7.42

Boston: 7.26

Baltimore: 7.21

St. Louis: 7.20

Minneapolis: 6.89

Pittsburgh: 6.84

Philadelphia: 6.73

San Francisco: 6.58

Chicago: 6.27

Portland, Oregon: 6.09

San Diego: 5.91

Seattle: 5.82

Detroit: 5.78

Los Angeles: 5.56

New York City: 5.37

Sacramento, Calif.: 5.35

Riverside, Calif.: 4.08