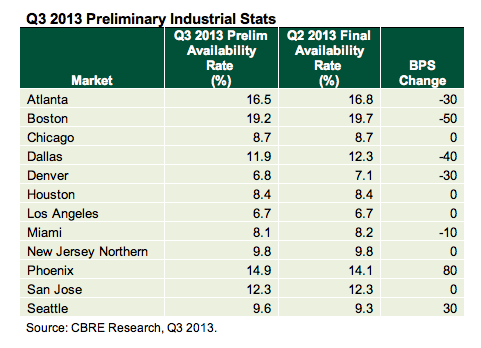

Just as the office market is tightening in North Texas, the industrial sector is performing well, too. CBRE is reporting third-quarter projected availability in the Dallas region at 11.9 percent. That’s a .40 improvement over the second quarter (12.3 percent)—and the lowest level the Dallas market has seen in more than a decade, reports Sara Rutledge, director of research and analysis for CBRE.

Just as the office market is tightening in North Texas, the industrial sector is performing well, too. CBRE is reporting third-quarter projected availability in the Dallas region at 11.9 percent. That’s a .40 improvement over the second quarter (12.3 percent)—and the lowest level the Dallas market has seen in more than a decade, reports Sara Rutledge, director of research and analysis for CBRE.

The declined in availability—defined as space that is actively being marketed and available for tenant buildout within 12 months—follows several years of strong net absorption and limited deliveries, Rutledge said. “Construction is rising, yet remains conservative relative to the vacancy rate and is largely tenant-driven, including two Amazon distribution centers,” she said.

Dallas’ .40 third-quarter drop is the second-largest in the country, second only to Boston, which saw its availability rate decline .50 from 19.7 percent to 19.2 percent. Demand there is largely coming from the food sector and smaller warehouse and distribution needs. In Dallas, it’s being driven by third-party logistics companies and e-commerce operations.

Brook Scott, CBRE’s interim head of research, Americas, said the U.S. industrial market is benefitting from consumer and business spending, a recovering housing market, and increased demand for logistics space tied to the growth of e-commerce.

Developers in the Lone Star State are responding in true Texas form. Dallas has 10.1 million square feet of industrial space under construction, and Houston as 7.8 million square feet.